This is the presentation of Dr. Paul Steinar Valle from Kontani, Norway in the Conference “Pangasius development in trade war” in the framework of Vietfish 2018.

Trade – a fair business …?

Pangasius is being «pushed away» from EU and US

It is competing with other whitefish cod, sole, haddock and pollock – with a lower price

Markets access for pangasius is claimed to be thwarted both by industry and media

Called «the whitefish wars» – due to among others claimed neg. environmental impact

Pangasius has been «framed» by negative claims – i.e. an alternative reality has been communicated and perceived

Rebuttals both by Aquaculture Stewardship Council (ASC) – and down the road by WWF (after first having added to the neg. publicity), have had little effect – so far.

WTO has formed a dispute panel to try to settle the differences between Vietnam and US

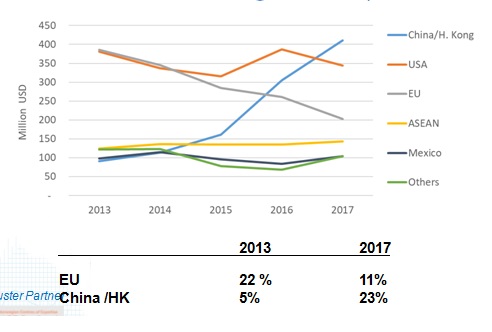

In the meantime, the Vietnamese sector has been working hard and pangasius is finding new markets in China, elsewhere in Asia and in Latin America.

Will Vietnam be «Third time lucky?» asked Gorjan Nikolik, Rabobank, at North Atlantic Seafood forum in Bergen earlier this year (Tom Seaman, Undercurrent News).

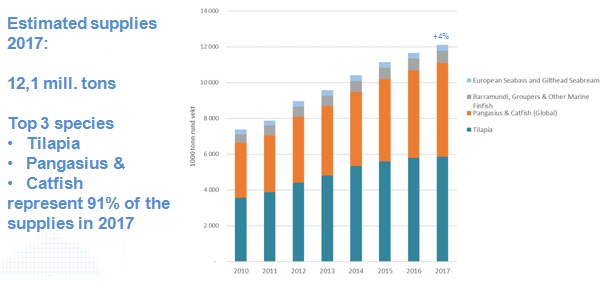

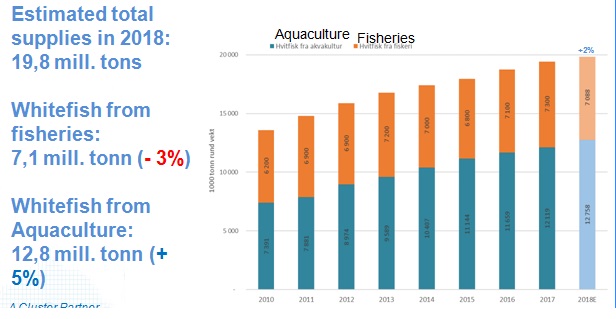

Supplies of whitefish from aquaculture

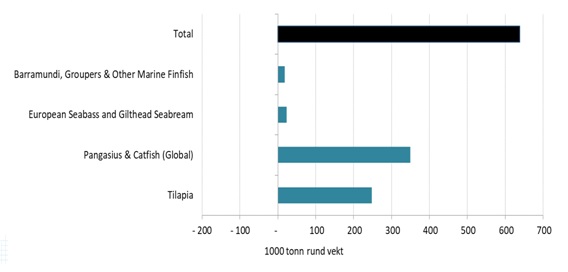

2017 – A moderate increase from 2016; Farmed whitefish

- A slow growth of Tilapia - China not contributing to growth….

- Increase for Pangasius & catfish-species – Vietnam not contributing

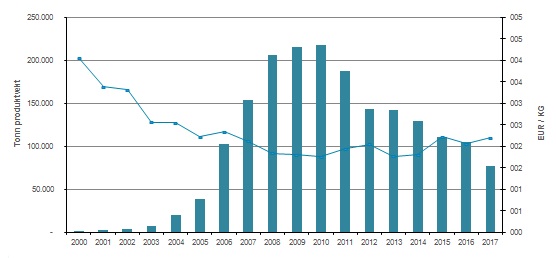

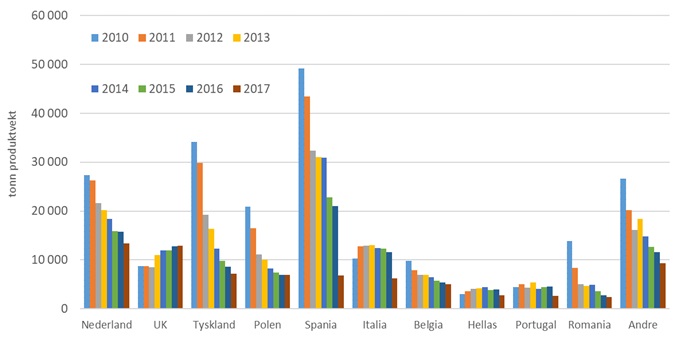

EU Imports of Pangasius

Frozen filles from Vietnam

Continiues decline since 2010 in EU

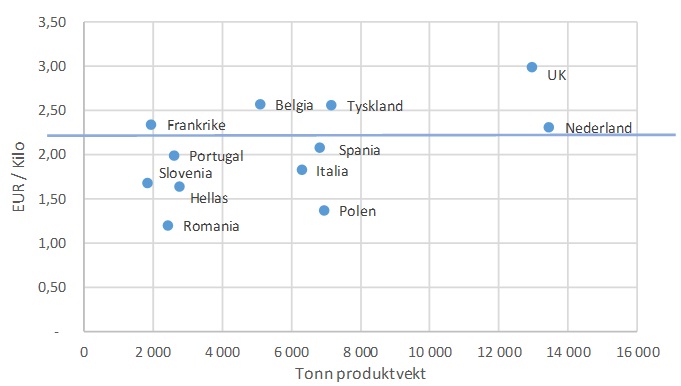

Markets for Pangasius in EU

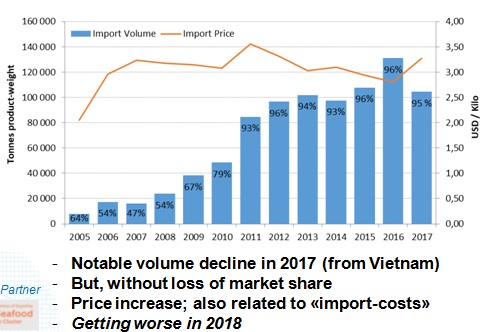

Pangasius – US Imports (Vietnam)

Frozen fillet presentations

Dramatic shift in direction of trade flow

Vietnamese Pangasius (Mill USD)

Estimated supplies of whitefish in 2018

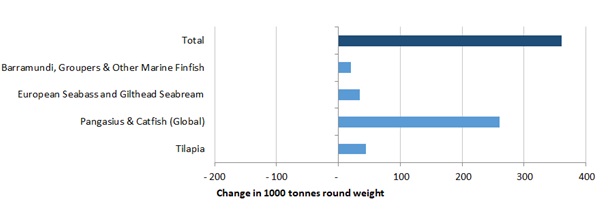

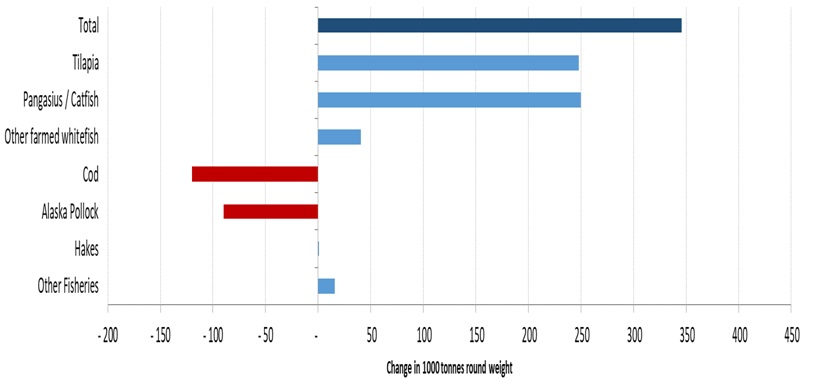

Estimated change in supplies of whitefish from aquaculture – 2017 to 2018 (by species)

Outlooks 2018 for selected Whitefish species

Marginal total volume growth – BUT shift towards more Aquaclture

- Farmed whitefish driving - «only a marginal» growth …

- Decrease in cod supply & pollock supply, - following cut in quotas

Outlook

2018; +5% increase in supplies of whitefish from aquaculture - -3 % from fisheries

Local markets AND China absorbs and steadily larger share of whitefish from aquaculture

Still significant drop in supplies of pangasius to EU and US - large volumes are routed to China and Hong Kong

Trends:

The growth in production in Asia will slow down

South-/Latin-America and Africa will be the growth regions

The Asia markets will continue to be strong – the flow of goods will «turn».

Europe need external seafood supplies

The EU seafood trade balance deficit is increasing – and –

EU pays more for the imported seafood year by year!

«Third time lucky…»(?) - and so what…?

Nikolik, Rabobank, criticized the pangasius sector for having a non-differentiated, basic product – competing «only» on price….?

Judged by reports from the Chinese market this might be changing – pangasius fillets are regarded as high quality products – sought for by Chinese consumers

However, differentiation and marketing is likely still a relevant focus to pursue!

Frame it – Market it – tell the story – in your own way – AND, expect what to come… because there will be health issues (for the fish), potential health risks (for the consumers) and potential environmental risks down the road

AND further, let us hope for a change to a more ethical and fair trade situation as discussed by Little et al. in Marine policy (2012) – both from a regulatory point of view, AND with respect to mass media.